Dividend Growth Investing & Retirement is supported by its readers through donations and affiliate links. If you purchase through a link on my site, I may earn a commission. Thanks! Learn more.

I am a dividend growth investor. I like to buy dividend paying companies with long track records of increasing dividends and strong competitive advantages. I look for higher than average dividend growth and a steadily increasing stream of income. Oh, and I also only like to buy when the stock is quite undervalued. This criterion has me waiting on the sidelines for prices to drop a lot of the time. I like to buy stocks, so it is difficult not to stray from my strategy with all this waiting around.

Cheap Options in the Gold Mining Industry

⭐ Find dividend growth stocks that have survived multiple recessions and increased dividends for 5, 10, 25+ years in a row.

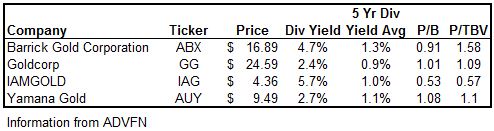

My most recent distraction has been the gold mining industry. The industry has been hit quite hard with the drop in gold prices. Gold mining companies typically pay out a small portion of earnings as dividends due to the higher capital costs associated with the industry. This usually translates into a low dividend yield that is below the 2.0-2.5% minimum entry yield I target. Because of the recent drop in prices, the dividend yield for a number of gold mining companies has risen above my minimum entry yield requirements. You can see from the below table that there are intriguing options out there.

Yamana Gold and Goldcorp offer dividend yield’s that are more than double their five year average annual yield’s. With price to book (P/B) and price to tangible book value (P/TBV) ratios close to 1.0 they offer compelling options. While these are compelling options, Barrick Gold Corporation and IAMGOLD appear to offer better value from a yield perspective.

Barrick Gold Corporation offers a whopping 4.7% dividend yield which is almost four times more than its 5 year average. Its P/B is below 1.0, but its P/TBV is quite higher coming in at 1.58. The other companies all have a P/TBV fairly close to their P/B, so from a price to book perspective it looks like there could be better options out there. Barrick Gold Corporation is a good example of how much prices have dropped. They recently had low prices that haven’t been seen for 10 years.

IAMGOLD

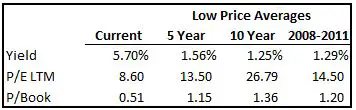

The company that has piqued my interest the most is IAMGOLD. From a value perspective it looks quite attractive. Its price to book ratio is 0.53 and its price to tangible book value is 0.57. With ratios like this it is easy to see why I’m interested. Not to mention it is currently yielding 5.7%, which is more than five times its five year historic average. Looking at more ratios compared to their averages based on low prices suggests that IAMGOLD is quite undervalued.

Morningstar currently rates this a five star stock when it is priced under $4.50, which would support an undervalued assumption. This company had me so interested that I put an order to buy shares for $4.50. A few hours later I ended up cancelling the order after realizing that it didn’t fit with my investment plan.

Why I’m Not Investing in IAMGOLD

It is not that I don’t think IAMGOLD is undervalued and that you could make decent capital gains from the stock. It’s just that it doesn’t meet my dividend growth criterion. I want companies with a wide economic moat. IAMGOLD is a mid tier gold mining company without a large competitive advantage. Gold companies’ earnings are controlled by the price of gold. This is why IAMGOLD’s EPS has been erratic from year to year. I want a company that has steadily increasing earnings. While IAMGOLD’s dividend yield is appealing, it doesn’t have a very impressive dividend streak and I don’t expect strong dividend growth in the future. For a lot of companies in this industry their dividend is tied to the price of gold, which is a hard thing to control. I want an increasing stream of dividends every year, not something tied to the price of gold.

Lessons Learned

In the past I have strayed from investing approach and I have been burned. A good example was my investment in Blackberry. What I’ve learned is that I should stick to dividend growth stocks with strong competitive advantages. It can be hard waiting around for prices to drop below my target prices and there will always be distractions like IAMGOLD out there. Sticking to your investment plan is important as changing strategies can be costly to investment returns. By focusing on my dividend growth strategy, I believe I will be able reach my financial freedom goals quicker.

Bottom Line

Find out what your investment goals are, come up with a plan to achieve them and stick with it.

Disclosure: I do not own any of the shares mentioned. See what is in my portfolio here.

Newsletter Sign-Up & Bonus

Have you enjoyed our content?

Then subscribe to our newsletter and you'll be emailed more great content from Dividend Growth Investing & Retirement (DGI&R).

BONUS: Subscribe today and you'll be emailed the most recent version of the Canadian Dividend All-Star List (CDASL).

The CDASL is an excel spreadsheet with an abundance of useful dividend screening information on Canadian companies that have increased their dividend for five or more years in a row.

The CDASL is one of the most popular resources that DGI&R offers so don't miss out!

![How to estimate dividend growth and total returns using Josh Peters’ Dividend Drill Return Model [Example & Spreadsheet]](https://dividendgrowthinvestingandretirement.com/wp-content/uploads/2018/10/How-to-estimate-dividend-growth-and-total-returns-using-Josh-Peters’-Dividend-Drill-Return-Model-Cover-768x575.png)