Dividend Growth Investing & Retirement is supported by its readers through donations and affiliate links. If you purchase through a link on my site, I may earn a commission. Thanks! Learn more.

As you know from my past few posts I’ve been reading Lowell Miller’s The Single Best Investment: Creating Wealth with Dividend Growth. One thing that surprised me a bit was his comments about inflation. The author pointed out that the 60 year average inflation rate in the United States is 4.1%. The book was written 8 years ago in 2006 and has a US focus, so I decided to do some of my own research to see if this figure was still accurate.

What is inflation?

Before I dive into the results, I want to explain what inflation is. Investopedia defines inflation as

“The rate at which the general level of prices for goods and services is rising, and, subsequently, purchasing power is falling.” […] “As inflation rises, every dollar will buy a smaller percentage of a good. For example, if the inflation rate is 2%, then a $1 pack of gum will cost $1.02 in a year.”

The Bank of Canada website has an inflation calculator that you can play around with to get an idea of how inflation affects your purchasing power. Here are a few of my results:

As you can see inflation over a long period of time has a significant affect.

Why inflation is important to dividend growth investors

Dividend growth investors who want to live off of their dividend income in retirement should be aware of inflation because their retirement expenses will cost more in the future. By investing in dividend growth stocks with dividend growth rates higher than inflation you are able to protect your purchasing power. This is just one reason why I love dividend growth stocks.

In order to protect your purchasing power it is important to invest in companies with dividend growth rates above inflation. Trying to guess what will happen in the future is impossible, but you can still make an educated guess based on historic inflation rates and central bank targets.

Central bank target inflation rates

Most countries today will try and target an inflation rate of 2-3% because this rate is considered beneficial for the economy. In the United States the Federal Reserve tries to “maintain an inflation rate of 2 percent over the medium term”1. This is similar to the Bank of Canada which “aims to keep inflation at the 2 per cent midpoint of an inflation-control target range of 1 to 3 per cent.”2

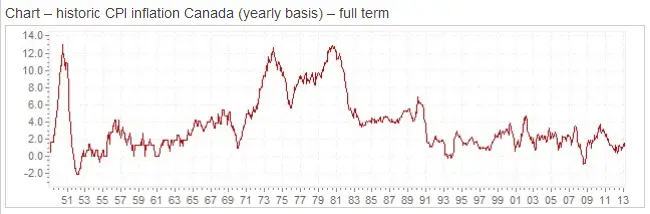

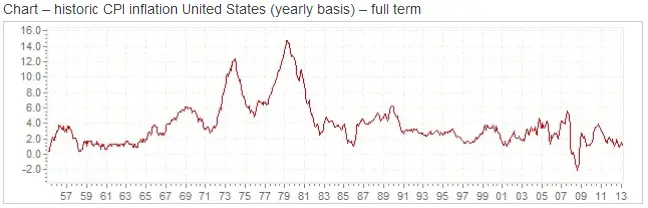

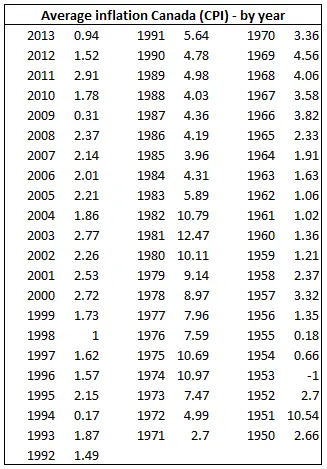

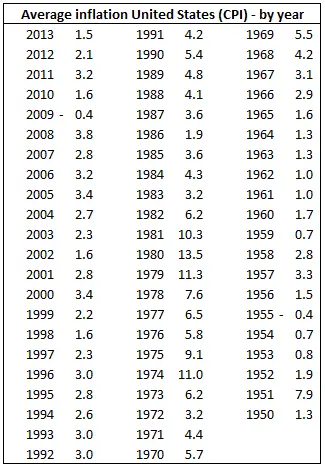

Historic inflation rates

It’s all well and good to have a target, but there are so many different factors that affect inflation that it becomes unrealistic to think that inflation will always be at the target rate. If you look at the annual inflation rates going back to the 1950s for Canada and the United States you’ll see that they have fluctuated quite a bit.

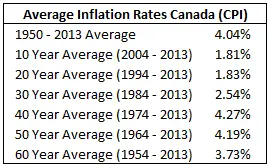

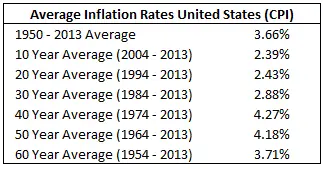

One noticeable trend is that the last 20 to 30 years have been much more stable than before that time. Looking at the 10, 20 and 30 year average inflation rates for both Canada and the United States in the tables below show that for the most part inflation has averaged around 2-3%. When you start looking at longer averages the rates increase to around 4%.

⭐ Find dividend growth stocks that have survived multiple recessions and increased dividends for 5, 10, 25+ years in a row.

For Canada the 60 year average is 3.73% and for the United States it is 3.71%. These are pretty close to the 60 year 4.1% average inflation rate mentioned in the 2006 edition of Lowell Miller’s The Single Best Investment: Creating Wealth with Dividend Growth. I like to be conservative in my estimates, so while in the past 20 to 30 years inflation has been around 2-3%, I prefer to use the longer term average of 4%.

How inflation affects your minimum dividend growth target

A lot of dividend growth investors want dividend growth from their investments to grow at or above inflation rates. With this approach they are able to protect their purchasing power, so come retirement their dividend income can support their expenses. With this in mind you would think the minimum dividend growth target would be 4%, but I prefer 6% as it gives you a bit of an extra cushion.

Say you invest in a company and dividend growth is projected at 6%. Fast forward a year and some negative event has occurred that the company has to recover from. Consequently their dividend growth ends up being lower than projected. With a target of 6% you have some extra room for those unexpected events. This is why 6% is my minimum dividend growth target.

In my portfolio I try and target 8% dividend growth, but I’ll still invest in a company if dividend growth is projected at 6%. As with most things in life, investing isn’t black and white and I find some flexibility is necessary. This is why I try and target 8% dividend growth, but will go as low as 6%. In a balanced portfolio you will have some companies that have high dividend growth in some years while others have lower growth. My goal is to average 8%. A good example of an instance where I’d accept 6% is a company with a high dividend yield. With these targets I feel like it provides good protection against inflation while also providing solid compounding returns.

How do you approach inflation in your portfolio?

Footnotes

Newsletter Sign-Up & Bonus

Have you enjoyed our content?

Then subscribe to our newsletter and you'll be emailed more great content from Dividend Growth Investing & Retirement (DGI&R).

BONUS: Subscribe today and you'll be emailed the most recent version of the Canadian Dividend All-Star List (CDASL).

The CDASL is an excel spreadsheet with an abundance of useful dividend screening information on Canadian companies that have increased their dividend for five or more years in a row.

The CDASL is one of the most popular resources that DGI&R offers so don't miss out!

My objective with my various accounts, both registered and non-registered, is to grow dividends by 10% year to year. Last year, 2012 to 2013, I managed 17%. Keep in mind that I am still working so I get to max out my RRSP contribution and I also max out my TFSA so that increases my principal above received dividends. All dividends are reinvested whenever I find a suitable dividends paying stock so that also increases dividends in the periods following the purchase. I am most active on stock purchases in Jan, Apr, Jul and Oct when the quarterlies come in. I will sell a stock at any time and that will affect some purchase timing if I do sell.

So far this year for five months I am running well above the 10% increase above last year’s dividends.

Sounds like you are investing in some solid dividend growth companies if you are getting 10-17% growth rates. What are some of the companies that have done well for you?

Everyone talks about inflation but the only time most people recognize it is when they see that their grocery bill, electric bill, property taxes, the price of gas, etc, etc all costing more. Sure some thing go down in price, but overall the rise in prices is up.

You did fantastic research and must have done a lot of work, but I like to take the government inflation rate and double it. This seem to work fairly closely to what I calculate the increases I’ve had to pay.

My overall dividend growth the past few years has been 6.5%. I have several holdings which have not increased their dividend (no cut and my YOC is high so I’ve not sold) so the others have had to make up the difference.

The other point on inflation is that it compounds, which means that the gum you said went from $1.00 to 1.02 next year, will cost $1.04, then 1.06, etc. More likely the increase would be from $1.00 to $1.05 if inflation is only 2% (hopefully so the company can provide a 5% increase in the dividend).

@DGI&R

COmpanies I still hold that are my major div payers BCE and IPL. Both have increased divs over the years with IPL presently paying me >18% on COP. PWF has been quite kind to me as well. VSN is quite nice at the price I bought in at. I have held CHE.UN and RUS but sold off on the upswing and re-invested. Have picked up substancial holdings in REITs of late with D, DRG and DIR (all .UN) being the major ones. They are up from my COP and pay quite nice.

Biggest loser was/is Nortel. Unfortunately I held some in my RRSP so that will be a wash out once the lawyers and accountants get paid off.

The only account I can really track is my LIRA as NO new money gets contributed to that account. It managed 17.8% dividend growth from 2012 – 2013. So that all comes from 1) dividend growth from individual stocks 2)re-investment of those dividends in to more stock and hence more dividends for the remainder of the year and 3) some selling and re-investment. This LIRA account has grown in value more than 10% per annum as it currently stands. Mind you, I probably would not have said that in 2009 but I did not sell out and the divs kept on rolling in and were re-invested.

Overall, for five months of 2014 I am currently at just over 17% div increase compared to six months 2013 and I still have the June divs to add in for 2014.

AHH! The miracle of compounding (and dividend increases)

you should consider a credit rating filter to your DGI ALL STAR LIST

Dividend growth is the best method I’ve found for the average person. A carefully selected portfolio contributed to over a couple of decades can really help towards financial independence.

I totally agree.

there was infaltion of 21% in 1992??

Oops, that is a typo. It should say 1.49, not 21.49. I’ve updated the table and article with the correct figure. Thanks for pointing that out.

Very well written again. Thanks for sharing it.

Even though its quite old. But I have to leave @^ comment for such a great Job.

Thanks!