Dividend Growth Investing & Retirement is supported by its readers through donations and affiliate links. If you purchase through a link on my site, I may earn a commission. Thanks! Learn more.

When I tell people I bought a Canadian bank stock recently, they naturally assume it’s one of the big six: Royal Bank of Canada [RY Trend], Toronto Dominion Bank [TD Trend], Bank of Nova Scotia [BNS Trend], Canadian Imperial Bank of Commerce CIBC [CM Trend], Bank of Montreal [BMO Trend], or National Bank of Canada [NA Trend]. They’d be wrong… as I bought Canadian Western Bank [CWB Trend] which is a smaller lesser known bank stock. In this dividend stock analysis I’ll go over what I like about this company so you can find out why I bought shares.

⭐ Find dividend growth stocks that have survived multiple recessions and increased dividends for 5, 10, 25+ years in a row.

Related Articles: The Great Canadian Banking Series: Bank of Nova Scotia Dividend Stock Analysis (Part 2 of 10), The Great Canadian Banking Series: Toronto-Dominion Bank Dividend Stock Analysis (Part 3 of 10), & The Great Canadian Banking Series: Royal Bank of Canada Dividend Stock Analysis (Part 4 of 10)

About Canadian Western Bank

Canadian Western Bank is a bank that operates mostly in Western Canada… go figure! Here is the description from Google Finance:

“Canadian Western Bank (CWB) is a bank offering a range of financial services. The Company operates in the financial services areas of banking, trust, insurance and wealth management. The Company and its operating affiliates, which are together known as Canadian Western Bank Group (CWB Group), offer a diversified range of financial services through approximately 41 banking branches, eight trust locations, two centralized insurance offices, a focused commercial equipment leasing centre and two wealth management locations. The Company’s operating companies/divisions include National Leasing, Canadian Western Trust, Valiant Trust, Canadian Direct Insurance, Adroit Investment Management, McLean & Partners Wealth Management and Canadian Western Financial. Canadian Direct Financial is a division of the Bank, while Optimum Mortgage is a division of Canadian Western Trust.”1

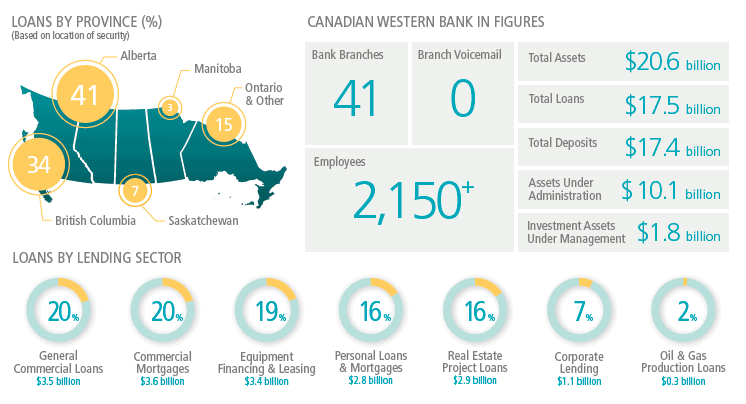

This is an OK overview of the business. I found that the 2014 Q4 Investor Fact Sheet2 on December 17, 2014 gave a better picture.

You can see that their main focus is in Alberta and BC with most of their loans (41%) coming from Alberta. The Albertan economy is reliant on the oil & gas industry so with the drop in oil prices recently (2nd half of 2014) it is easy to understand why Canadian Western Bank’s price has dropped too.

10 Year Stock Chart (December 17, 2014)

Looking at the 10 year stock chart, there is a 10 year annual average return of 9.6%. If we include the dividend payments over the past 10 fiscal years (Total dividends paid of $4.72) then the total average annual return would be 11.2% with the average return from dividends representing 1.6%.

Overall pretty decent returns. You can see the effects of the financial crisis on the stock price in 2008 and 2009 which is expected for most bank stocks.

Revenue & Earnings

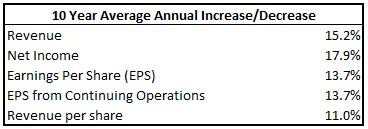

In the case of Canadian Western Bank I get the following growth rates based on the most recent fiscal period end (October 31, 2014).

All annual growth rates are above the 8% I typically like to see so I’m happy. I was perusing the website to learn more about the company and a milestone they achieved in 2013 jumped out at me from their “About Us” page3.

In 2013 “CWB celebrates 100 consecutive profitable quarters”3

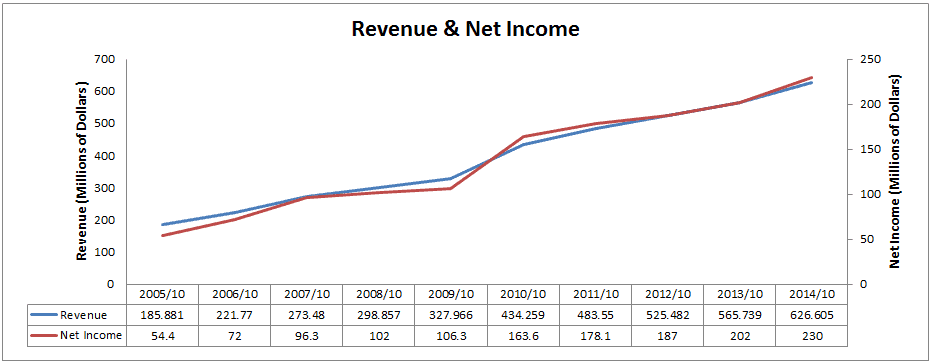

I like to see that a company hasn’t lost money in the past decade and has consistently increased their earnings. This bank has been profitable in each quarter for over 25 years which is even more impressive. You’ll see from the charts below that they’ve also managed to increase earnings consistently.

In the past decade the company has managed to increase both revenue and net income every year. This is quite impressive as most companies will have a blip or two from a hard year. Considering this is a bank stock I was surprised to see that they increased revenue and net income in 2009 from 2008 in the height of the financial crisis. Granted it wasn’t much higher, but still.

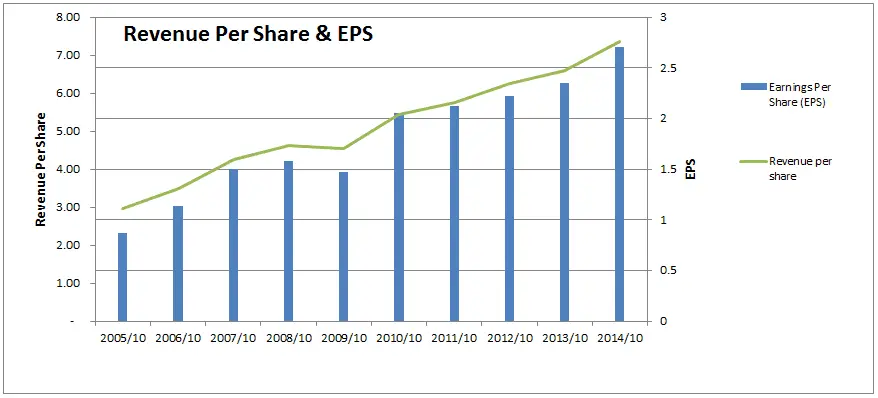

With the earnings per share (EPS) and revenue per share chart below we get a similar trend.

Unlike the previous revenue and net income chart EPS and revenue per share dropped in 2009 as a result of additional shares being issued. Other than this small drop in 2009 from the financial crisis they have managed to steadily increase revenue and earnings per share at a good clip and in a consistent manner.

Consistent and growing earnings each year at high growth rates is ideally what I look for and Canadian Western Bank has managed to do this. Good news so far, let’s look at dividends next.

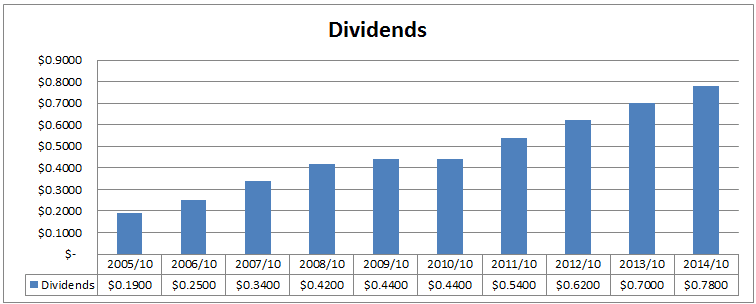

Dividends

A quick look at the Canadian Dividend All-Star List and I can see that Canadian Western Bank has increased their dividend for 22 consecutive calendar years in a row. This is an impressive streak. You’ll notice if you look at the Dividends chart below that in fiscal 2010 they kept the dividend the same as the prior year, but because the Canadian Dividend All-Star List looks at the calendar year for each company the dividend streak was maintained from a calendar year perspective.

The big 6 Canadian banks all kept their dividend steady during the financial crisis too, but Canadian Western Bank returned to increasing dividends before the big 6 as it was able to recover quicker and had a lower payout ratio.

The most recent dividend increase was announced earlier this month (December 2014). They increased the quarterly dividend from $0.20 to $0.21 which was a 5.0% increase. Since 2011 they have been increasing their dividend twice a year, so the annual increase is actually from $0.19 to $0.21 which is a 10.5% increase. With this announcement it will mean that so in 2015 their dividend streak will increase to 23 years in a row.

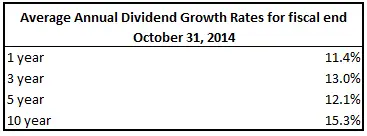

Other than the blip in 2010, I’m happy with the dividends over the past decade and if you look at the average annual growth rates below you’ll see why.

All the dividend growth rates are easily above the 8% I like to see. More good news, but is it sustainable?

Dividend Sustainability

The 10 year average annual dividend growth has been slightly above EPS growth which would suggests a sustainable dividend, but eventually dividend growth may slow down a bit to match earnings growth.

Let’s take a look at the payout ratio to see how much room for growth the dividend still has.

Looking at the past 10 years it looks like they have been targeting a payout ratio of between 20-30% which is actually lower than the big 6 banks which usually pay out around 40-60%. A lower payout ratio is a plus as it provides for more flexibility when times get tough. This is probably why Canadian Western Bank was able to start increasing their dividend before the big 6 after the financial crisis.

The company has been increasing dividends slightly faster than earnings, but because they have a low reasonable payout ratio the dividend appears sustainable. Typically I look for a payout ratio below 60% and they are well below this which is good.

Estimated Future Dividend Growth

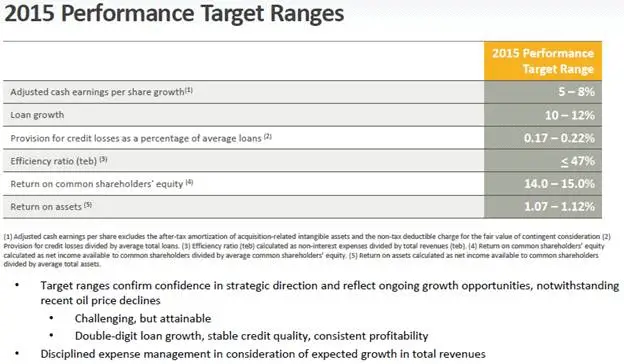

When they announced their most recent dividend increase as part of the December 4, 2014 Q4 2014 Results Earnings Conference Call they explained that they “expect to remain near the top end of our target payout ratio of 25% to 30% of net income available to common shareholders.” As part of this conference call they provided 2015 performance target ranges in their investor presentation which have helped me estimate the dividend.

The 2014 fiscal end payout ratio was 28.9% which is near the high end of their 25% to 30% ratio target. As they are already near the higher end of the range I would expect dividend growth for 2015 to be roughly in line with their EPS share growth target of 5-8%.

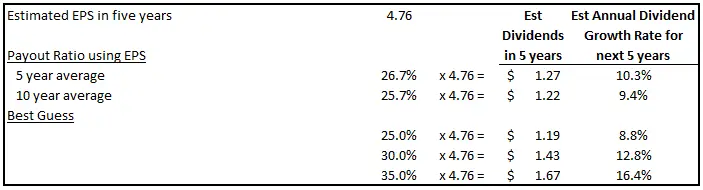

According to Yahoo Finance on December 17, 2014, analysts are estimating earnings growth of 12.6% for the next 5 years. Using a 12.6% growth rate would result in EPS of $4.89 in 5 years’ time which we can use to estimate future dividend growth.

Using the above assumptions and a payout ratio or 25% to 30% you can expect dividend growth around 9% to 14% which is a good dividend growth rate and above the 8% I like to see. With the uncertainty in oil prices and how it will affect Alberta and Canadian Western Bank I think it’s safer to assume that dividend growth in 2015 could be lower than this around their target earnings growth of 5-8%. Ultimately I expect dividend growth to be in line with EPS growth as they are near the top of their 30% payout ratio target.

In the very long term I could see them increasing their payout ratio target to become more in line with the big 6 banks which are around 40% to 60%. If this were to happen then dividend growth could sustainably grow above EPS growth, but this is not something I expect to happen anytime soon.

Bottom line, dividend growth prospects look good, but there is uncertainty related to oil prices looming which could affect earnings.

Related article: Can Past Dividend Growth Rates Be Relied Upon To Predict Future Rates?

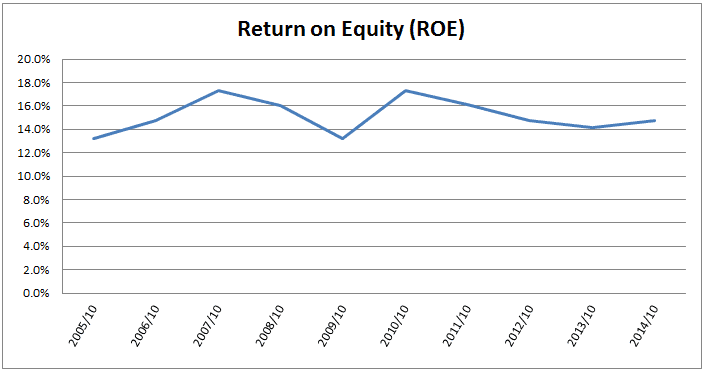

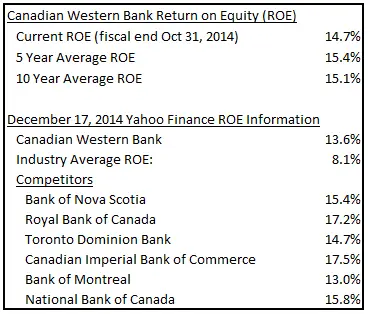

Competitive Advantage & Return on Equity (ROE)

I would say that the big 6 banks have most of the competitive advantage in the Canadian market, but Canadian Western Bank holds its own. I wouldn’t say it has a wide moat, but I think it does have a narrow one. Morningstar doesn’t rate them anymore, but when they did back in 2009 they also gave a narrow moat rating.

ROE has been around 13% to 17% over the past decade with it averaging around 15%. This is pretty good, but not great. Consistently at 20% or higher is great. While they may not have 20%, they are still doing well compared to the other big banks, so from an industry standpoint they are definitely keeping up with the big boys.

The industry average for Money Center Banks is 8.1% according to Yahoo Finance, but I think this looks at mostly US companies which Canadian Western Bank isn’t competing with, so I’d take this with a grain of salt.

Financial Strength

Assessing the financial strength of banks can be complicated, so I usually rely on the rating agencies for their take. Canadian Western Bank has this information available on their website4 which is convenient.

Overall when I look at the ratings above I would say that they have good financial strength and I’d be willing to invest in them. It could be better, but overall it is good. In the above case the debt is rated by DBRS, so I’d generally want to see BBB (high) or higher. If S&P has done the rating I’d look for BBB+ or higher.

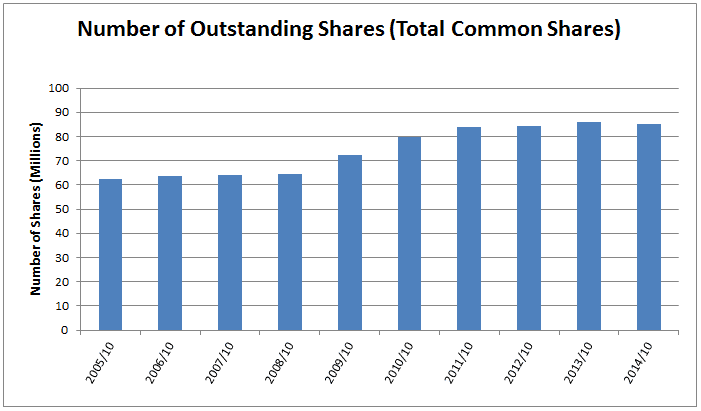

Shares Outstanding

I don’t place too much importance on share buybacks in my analysis. Given the choice I’d rather have a company that increases its dividend versus buying back shares, but often the companies I look at are doing both. A decreasing number of shares outstanding is a good thing, but I like to see smart share buyback programs. That is I like to see a company buying back its shares when they are priced low, rather than just buying back for the sake of buying back.

In Canadian Western Bank’s case shares outstanding have increased a bit over the past decade. This increase in shares is why the EPS and revenue per share growth rates were slightly lower than the revenue and net income growth rates. Because the EPS and revenue per share growth rates were still good I’m not worried that the share count increased.

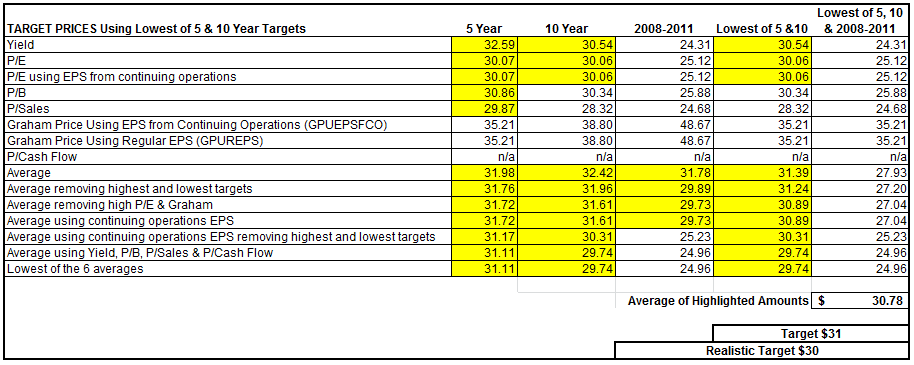

Valuation

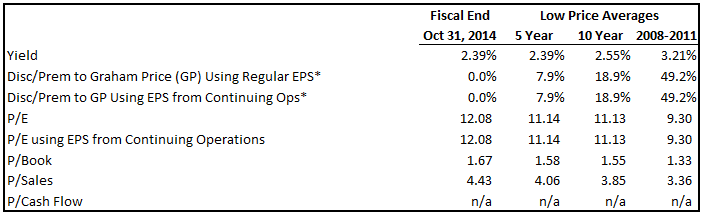

I use 6 main ratios to determine a fair price: Yield, Discount/Premium of the low price compared to the Graham Price, P/E, P/B, P/Sales and P/Cash flow. I like to look at both EPS and EPS from continuing operations so it ends up being a total of 8 ratios as the Graham Price an P/E both use EPS. You can read more about my valuation method here.

I get the following for Canadian Western Bank. I wasn’t able to get reliable cash flow per share information, so it wasn’t calculated.

* The discount or premium to Graham Price hasn’t been calculated in the normal fashion. For the details read this article.

In the table above you can see that at the fiscal end (Oct 31, 2014) the stock was starting trade around its historic lows when looking at various valuation measures. As of writing (December 17, 2014) it has dropped in price further which is enticing. Next I’ll try and figure out a price I’d be willing to buy at.

Target Buy Price

I use the averages from the previous table to determine my target price. Using these averages creates a lot of different target prices, so I back-test this strategy over the past 10 years. I identify which of the 8 valuation techniques would have given me a chance to buy the stock in two to three fiscal years in the past 10 fiscal years. It’s not always possible to test my strategy back 10 years, due to limited financial information, but I do my best. The results are highlighted below.

The target price comes out at $31, but I lowered it to $30 because I wanted a slightly higher dividend yield. With the $0.21 quarterly dividend the dividend yield at $30 is 2.8%. Compared to the big 6 banks, 2.8% is low comparatively, but I think you can expect higher dividend growth. Look back to 2003 and you’ll notice that only in two other years; 2008 and 2009, was the dividend yield higher than it is now. This is a good indication of value.

Conclusion

Overall I like this company for its consistency. They just seem to make more and more money over time and at high growth rates. This translates into a high dividend growth rate which has led to a long dividend streak of 22 soon to be 23 years. Granted the dividend yield offered compared to the big Canadian banks is lower, but I think Canadian Western Bank will offer better dividend growth with the added benefit of a lower payout ratio.

With the recent drop in price below my target buy price of $30, I purchased shares. On December 16, 2014 I purchased shares of Canadian Western Bank for an average price of $29.33 after the broker commission was paid. Read about my portfolio changes here and see what’s in my portfolio here.

There is some uncertainty in the market because oil prices have dropped so much recently which in turn has affected Canadian Western Bank’s price. I don’t know where oil prices will go, but if they keep dropping than I’d expect Canadian Western Bank’s stock to keep dropping too. I’ve found that buying stocks when they appear cheap is a good long term strategy, so I’ll stick with it even with the added uncertainty in the market right now.

I’ve talked about the big six banks and I just wanted to clarify that I’d love to own some of the big six banks too, but Canadian Western Bank has been the first bank stock to drop below my target buy price since I started rebuilding the portfolio after the condo purchase.

Related article: I Bought A Condo – Excitement & Worries

What do you think of my purchase of Canadian Western Bank?

Footnote links

1 http://www.google.ca/finance?cid=665836

3 http://www.cwbankgroup.com/about-us/who-we-are

4 http://www.cwbankgroup.com/investor-relations/debt-security-information

Photo credit: bmward_2000 / Foter / CC BY-NC

Newsletter Sign-Up & Bonus

Have you enjoyed our content?

Then subscribe to our newsletter and you'll be emailed more great content from Dividend Growth Investing & Retirement (DGI&R).

BONUS: Subscribe today and you'll be emailed the most recent version of the Canadian Dividend All-Star List (CDASL).

The CDASL is an excel spreadsheet with an abundance of useful dividend screening information on Canadian companies that have increased their dividend for five or more years in a row.

The CDASL is one of the most popular resources that DGI&R offers so don't miss out!

Thanks for sharing the analysis/

Very well thought out and written analysis.

That’s a good general analysis and I hope you do very well with this investment. Banks are risky because they are, by nature, extremely leveraged. For example CWB sales only represented around 3% of total assets last year (all numbers from M*). Even with profit margins of ~35% they needed to have about $13 in assets for each $1 in equity to achieve the ROE The value of the Assets then are going to be of supreme importance in the valuation of banks. Even a slight degradation in asset value, through defaults, bankruptcies etc, could wipe the bank out or give them a very rough ride.

Therefore I think price to book, or even better price to tangible book value should be given a much higher priority in any bank analysis. My back of the envelope calculations show that price to tangible book value will be 1:1 when CWB hits around $19-20 per share, at which point I think it would be an interesting opportunity (all else the same). During the 2008-09 crises this stock changed hands for around 3/4 of tangible book value which would make it even more interesting.

If it drops to $19-20 I’d be quite happy to pick up some more shares.

Do you like to get to 1:1 book value with all bank stocks before you invest, or are you just talking about CWB in this case.

Cheers,

DGI&R

With the oil price situation, Canadian banks are more risky than before. It’s still safe enough to buy in my point of view, especially with a long-term strategy in mind.

I agree. The Canadian Banks have come down in price quite a bit recently so I’m getting more interested now. I’ve been looking at Bank of Nova Scotia, TD, and National Bank, but I need them to drop more before I’d buy. Bank of Nova Scotia is currently the closest to my target buy price.

BNS is probably also the best buy! 😉

Hit the button too fast! 😉 But it might be National Bank’s year in 2015! It’s in my top 3 for Canadian!

Any updates on your above analysis?

They just announced a 5% dividend increase. Quarterly dividend will be $0.22 now.

I know this analysis is a little old, but has your positioned changed much. With CWB stock price down to 24.59, would you be willing to increase your position? With the uncertainty of when oil prices will rise more significantly, and the canadian housing market being questioned, does it change your opinion on Canadian banks?

I bought CWB at $29.31, then averaged down at $26.93 and then again at $24, but this was back in 2015. Because of these additional purchases I already have a high exposure to CWB and I don’t plan on adding more to the company at this time unless there is a significant drop. I have a high exposure to financials so I’m trying to limit my purchases in this sector. For CWB my expectations for dividend growth have lowered, but I still like them as a company.

With the recent decline in CWB.TO share price would you consider increasing your position?